Driving professional standards

Annual Report 2022

Melissa Collett, former Professional Standards Director, shared her thoughts with us on the progress made by the CII in building a trusted profession in 2022, and her team’s focus in the year ahead.

How did you promote professional standards and Chartered during 2022?

How did you promote professional standards and Chartered during 2022?

We continued to promote the value of corporate Chartered status, for example through participating at conferences such as the British Insurance Brokers’ Association Conference, the St James’s Place Chartered Symposium, and the Managing General Agents Association Conference – and the number of individuals working within a Chartered firm continued to grow with a 3.2% year-on-year growth in employees in Chartered firms in January 2023.

What progress has the CII made in promoting Chartered status in the period?

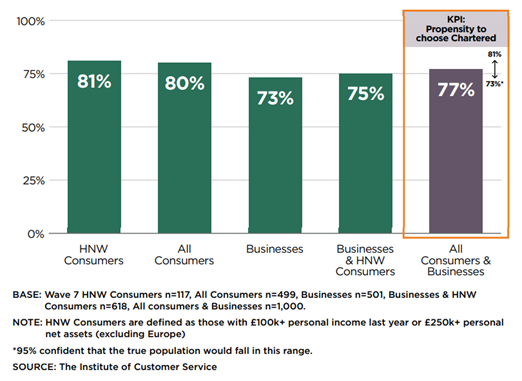

Our commitment to promoting the value of Chartered status is demonstrated by the appointment of a new Chartered marketing executive to focus on enhancing the visibility of the Chartered badge and helping firms promote their Chartered status. During 2022 we refreshed our Chartered toolkit with new videos and content, and we have showcased achieving Chartered status by spotlighting new Chartered firms on social media, in the press and on our website. We continue to independently measure public perception of Chartered status through the Institute of Customer Service, and in the second half of 2022 it showed that 77% of businesses and consumers would choose a Chartered firm over a non-Chartered one – our highest ever result (up from 75% in the first half of the year). It is good to see the positive results of our efforts to promote and enhance the credibility of corporate Chartered status.

Key metrics: Propensity to choose

In wave 7, 77% of Consumers and Businesses would be more likely to choose a firm with Chartered status, slightly up from Wave 6 (75%). This marks the highest level recorded to date.

If you were looking to get professional financial or insurance advice, what type of firm would you be more likely to choose? A firm with Chartered status – HNW Consumers, All Consumers and businesses.

- Despite a fall in the number of businesses and HNW consumers to choose a firm with Chartered status, the overall propensity to choose a Chartered firm is 2 percentage points higher than wave 6

- 80% of all consumers report they would be more likely to choose a firm with Chartered status, up by 5 percentage points from wave 6

Were your plans for professionalism included in the Shaping the Future Together consultation

The proposals for professionalism formed a major part of the Shaping the Future Together consultation, both around member certification and the Chartered ethos for individuals.

The proposals for professionalism formed a major part of the Shaping the Future Together consultation, both around member certification and the Chartered ethos for individuals.

The feedback showed that practitioners support greater professional accountability and a focus on Chartered status, and “highest professional standards” is now a key pillar of the CII’s new Strategic Plan.

How are you working to balance the needs of members with consumer and regulatory expectations to continue to raise professional standards?

We continued to discuss key proposals with the regulator this year. We are keen to demonstrate that Chartered status aligns with and supports regulatory requirements such as the Consumer Duty, which came into force in July 2023. We sought the regulator’s input into our consultation proposals around professionalism and sought to understand from its perspective why, unlike financial advisers, insurance advisers have no requirement for qualifications. We continued to seek information from the FCA about which firms faced enforcement action and business failure as a result of providing poor advice around pension transfers. The intention of this work is to protect the reputation of our professional community, including Chartered individuals and firms.

How have you supported members to raise public trust in the profession?

This year saw the publication and promotion of Green Finance: a Companion Guide to the Code of Ethics. This is part of our series of companion guides to the CII’s Code of Ethics. Protection of our natural environment is a global concern. Our Green Finance Companion Guide gives members guidance about how to incorporate green finance-related thinking into their decision-making, and sets out their need to act as role models when it comes to sustainability. It has a foreword from Lloyd’s and complements our new Certificate in Climate Risk, developed in conjunction with the Chartered Body Alliance, of which the Institute is a proud member.

This year saw the publication and promotion of Green Finance: a Companion Guide to the Code of Ethics. This is part of our series of companion guides to the CII’s Code of Ethics. Protection of our natural environment is a global concern. Our Green Finance Companion Guide gives members guidance about how to incorporate green finance-related thinking into their decision-making, and sets out their need to act as role models when it comes to sustainability. It has a foreword from Lloyd’s and complements our new Certificate in Climate Risk, developed in conjunction with the Chartered Body Alliance, of which the Institute is a proud member.

How is your team supporting and promoting the EDI agenda through your work?

We continue to support Chartered firms in enhancing their EDI cultures. In 2019 the CII introduced a new requirement for all CII Chartered firms to have an equality, diversity and inclusion (EDI) policy in place. In return, the CII committed to measure the impact these policies have and to share the findings and examples of good practice within the corporate Chartered community. We surveyed Chartered firms in 2021 and had a response rate equivalent to 40% of all Chartered firms, and the findings around leadership, accountabilities and inclusive cultures showed that good practice around EDI is being embedded in Chartered firms. In 2022 we built on that by delivering a number of webinars and articles in The Journal and we hope to see the fruits of that guidance in our next Chartered firm EDI survey planned for 2023.

What other work would you point to, including Internationally, during the period?

We also delivered a significant amount of thought-leadership and CPD content on professional standards throughout the year. This reaches thousands of professionals, through articles in The Journal and Personal Finance Professional and industry press, podcasts on CII Radio, and presenting at conferences hosted by the CII’s own Professional Focus series, Local Institutes, BIBA, COVER, MGAA, Lloyd’s Dive In Festival, Women in Insurance, and events to celebrate International Women’s Day, amongst others. We were recognised globally for thought-leadership on digital ethics, AI and insurance by being invited to speak on various panels on AI, including Insurtech events with an international audience.

We also delivered a significant amount of thought-leadership and CPD content on professional standards throughout the year. This reaches thousands of professionals, through articles in The Journal and Personal Finance Professional and industry press, podcasts on CII Radio, and presenting at conferences hosted by the CII’s own Professional Focus series, Local Institutes, BIBA, COVER, MGAA, Lloyd’s Dive In Festival, Women in Insurance, and events to celebrate International Women’s Day, amongst others. We were recognised globally for thought-leadership on digital ethics, AI and insurance by being invited to speak on various panels on AI, including Insurtech events with an international audience.

Dr Matt Connell, Director of Policy and Public Affairs, updated us on improvements to, and results from, the Public Trust Index and how The CII has sought to influence public policy during the year.

Dr Matt Connell, Director of Policy and Public Affairs, updated us on improvements to, and results from, the Public Trust Index and how The CII has sought to influence public policy during the year.

What improvements have you made to the Public Trust Index during the period?

The format and the questions are still the same, but we are delving deeper into what’s going on day to day. So, rather than just saying consumer satisfaction’s gone up by 2% or down by 2%, we are trying to understand and communicate what’s driving the outcomes.

What factors are driving the level of public trust in insurance currently?

Household budgets are clearly squeezed currently due to the increase in the cost of living. However, insurance premiums have stayed relatively stable while other costs have skyrocketed, putting insurance in a better light in comparison with other providers.

There is, however, a greater focus from consumers on the speed and manner in which claims are processed. A good example of progress in this area was during the pandemic when many insurers made a partial payment up front to let claimants retain control of their lives or businesses, while they processed the ins and outs of the full claim – a move praised by the FCA.

The SMEs satisfaction rate has gone up, so the issues with business interruption overall haven’t contaminated trust in the profession too badly. Obviously, there are some test cases that still need to be resolved but overall, in terms of the public perception of the sector, it hasn’t festered too much.

Lastly, at the beginning of 2022, the FCA introduced rules about new and existing customers and treating them the same, and although that hasn’t really fed through in terms of perceptions yet, people are still very wary about how insurers behave with renewal pricing, and that’s particularly true for retail customers.

What examples can you point to where the CII is seeking to influence regulatory policy?

Under MiFID rules, in a falling market, advisers used to have to contact their clients to tell them that the market had fallen by a certain amount. It was a massively counterproductive piece of regulation that was onerous for advisers and did the opposite of what clients needed to happen by increasing their anxiety rather than reassuring them. So, in lockdown we asked the FCA to temporarily suspend the rule. At the end of 2022, HM Treasury decided to make the suspension of the rule permanent, and that is in the process of being made law as part of a wider piece of reform on financial services.

Looking forward, on sustainability we’re doing quite a lot. As Melissa mentioned, we’ve just published Green Finance: a Companion Guide to the Code, which goes into more detail about the ethical issues around sustainability. We’re also doing a piece of work with the FCA and the Green Finance Education Charter, which is a group of professional bodies spanning banking, investment, insurance, accounting and actuarial, looking at what all the different financial professions should be doing to link with each other. We’re leading the piece on insurance and that’s going to be fed into the FCA’s continuing work on regulation around sustainability, biodiversity, and diversity and inclusion.