Just say no to negative real yields

Technical Article

Publication date:

29 January 2019

Last updated:

19 February 2026

Author(s):

Technical Connection, Terence Moll

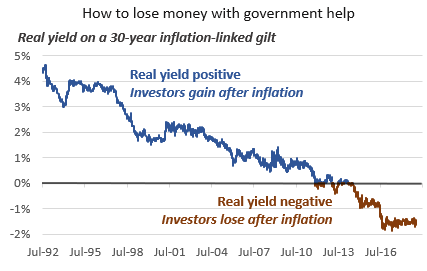

Her Majesty’s government has a special deal right now. Give the Treasury £100 and in 30 years’ time you will receive £64.36 back, allowing for inflation. Investors can’t get enough of it.

This may sound like a bad joke, but it isn’t. The product in question is the 30-year inflation-linked gilt, whose real yield is currently -1.46% (see graph). If you 'invest' in it, you will lose 1.46% of the real value of your investment every year.

Who would be crazy enough to buy a product that the Treasury guarantees will lose one third of its real (inflation-adjusted) value over 30 years? Who is responsible for one of the most remarkable distortions in the world of finance? The answer is simple; pension funds.

The UK’s defined-benefit pension schemes had liabilities of £1.8 trillion in March 2018, which are linked to inflation by various government rules. They hoover up products like inflation-linked gilts that help them to manage their interest rate and inflation risk – at the cost of losing their pensioners lots of money in the long run.

Hedging against inflation

Once upon a time, inflation was the great enemy of the investor. In the 1970s and 1980s the major goal was to find investments that could beat inflation, which peaked at 26.9% in August 1975, and spiked up to 10.9% in October 1990.

Index-linked gilts were developed to protect investors from the erosive effects of inflation. In the mid-1990s the yield on a 30-year index-linked gilt was 4%, so investors were guaranteed to triple the real value of their money by the year 2025. If you expected to retire in 30 years you could buy a 30-year index-linked gilt whose value was guaranteed to move with the Retail Price Index, thus protecting your savings against inflation and giving you a generous real return too.

Those days are a distant memory. Index-linked gilts have been offering negative returns for several years now.

And conventional government bonds also look unpromising. The 10-year gilt yield is 1.3%, for example, which is below Consumer Price Inflation at 2.1%.

Like the Bank of England, we expect UK consumer inflation to average around 2% per year over the next 10 years. In that case, investors in 10-year gilts can expect to lose 6% in real terms if they hold the bond until maturity.

Government bonds have traditionally been the bedrock of defensive investing, providing inflation-beating returns to investors and often performing best when economies slowed and equities were weak. At current interest rates, though, we expect gilts to fall in real terms in most economic scenarios.

By contrast, long-term equity investors can expect to beat inflation, even if the ride is wilder. The FTSE 100, for example, currently offers a dividend yield of almost five percent, which is high by historical standards and far ahead of inflation. And we expect the sales and earnings of its companies to rise by more than inflation over time, which should provide investors with capital gains in due course.

This document is believed to be accurate but is not intended as a basis of knowledge upon which advice can be given. Neither the author (personal or corporate), the CII group, local institute or Society, or any of the officers or employees of those organisations accept any responsibility for any loss occasioned to any person acting or refraining from action as a result of the data or opinions included in this material. Opinions expressed are those of the author or authors and not necessarily those of the CII group, local institutes, or Societies.